A speeding ticket isn’t just a fine-it’s a mark on your driving record that can follow you for years. The speeding consequences extend far beyond the initial court costs, affecting your insurance rates and your ability to drive safely.

At floridadetscourse.com, we’ve seen how a single violation can snowball into serious financial and legal complications. Understanding what happens after you get a ticket is the first step toward protecting your record and your wallet.

How Your Driving Record Changes After a Speeding Ticket

Points Stack Up Fast and Create Real Consequences

Most states assign points to your license when you receive a speeding ticket, and these points represent a direct measure of driving risk in the eyes of law enforcement and insurance companies. The number of points varies significantly by state and the severity of the violation. Arizona adds 3 points for speeding, while other states assign different values depending on how far over the limit you were driving. Accumulate points within 12 months, and you’ll face traffic school requirements or license suspension-creating an immediate threat to your ability to drive legally. The problem intensifies when you receive multiple violations because points stack up quickly, and once you hit your state’s threshold, you face real consequences beyond just higher insurance premiums.

Points Expire, But Insurance Impact Lingers Much Longer

Points don’t stay on your driving record forever, but they persist long enough to damage your finances. Most states keep points for 1 to 3 years, though some extend this timeline depending on the offense. The critical issue is that even after points expire from your driving record, the underlying conviction remains visible to insurance companies. Insurance impact lingers after points expire, with a speeding ticket remaining on your insurance record for a minimum of three years, depending on your state and the insurer. Insurance companies set their own timelines for how long they consider violations, which often extends beyond the state’s point expiration period. You should check your state’s DMV website to confirm your specific timeline, but don’t assume that points disappearing means your insurance problems are over.

Multiple Tickets Within Three Years Multiply Your Financial Damage

A single speeding ticket might not tank your rates, but two or more tickets within three years virtually guarantees a significant increase. Bankrate found that the rate increase scales with the severity of violations-higher speeds over the limit and repeat offenses produce bigger surcharges. If you’re caught going 16 mph over the limit once, you might see a modest increase, but a second ticket within three years could push your premium up by 22% or more according to Bankrate’s November 2025 data. The cumulative effect matters because insurers view repeat violations as a pattern of risky behavior rather than a one-time mistake. This pattern of escalating consequences is why your first ticket demands immediate action to prevent a second one-the financial damage multiplies rapidly with each additional violation, and understanding this reality helps you make better decisions behind the wheel.

What Does a Speeding Ticket Actually Cost

The Initial Fine Is Just the Starting Point

A $200 fine at the courthouse marks only the beginning of what a speeding ticket costs you. Court costs add another layer depending on your state, sometimes ranging from $50 to $200, plus administrative fees that vary by jurisdiction. Some states also impose additional surcharges or assessments that appear on your fine notice, and failure to pay promptly triggers late fees that compound the damage. The financial hit extends far beyond the initial ticket because insurance companies don’t just raise your rate for one year-they typically penalize you for three to five years depending on your state and insurer.

Insurance Rate Increases Dwarf the Original Fine

The real financial damage emerges months later when your insurance company reviews your driving record at renewal and raises your rates. According to Bankrate’s analysis, a single speeding ticket increases your annual premium by an average of 23% for full coverage, which translates to roughly $759 more per year on a typical $3,299 annual policy. That $200 ticket becomes a $2,277 expense over three years when you factor in the insurance surcharge alone. Insurance companies don’t just raise your rate for one year-they typically penalize you for years depending on your state and insurer.

State Location and Speed Severity Create Dramatic Variations

The severity of your rate increase depends directly on how fast you were going and where you live. Bankrate found that state-by-state variations are dramatic: California drivers see roughly a 39% increase after a speeding ticket, while Florida drivers experience around an 8% rise. North Carolina pushes closer to 50%, which means some drivers face premiums exceeding $4,900 annually after a single violation. Going 16 mph over the limit produces a smaller increase than going 30 mph over the limit. Multiple violations within three years escalate the problem exponentially because insurers view repeat violations as proof of dangerous behavior rather than a mistake.

Shopping for New Insurance Saves Hundreds of Dollars

Different carriers price risk differently, and some insurers penalize speeding tickets more harshly than others. Bankrate’s data shows that carriers like Auto-Owners, Erie, USAA, Geico, and Nationwide tend to offer lower post-ticket premiums compared to the national average. Comparing quotes across at least three insurers can save you hundreds of dollars annually. Losing your safe-driving discount amplifies the damage-if you qualified for a discount before the ticket, you’ll lose that benefit immediately, which compounds the rate increase beyond the base surcharge itself.

Your Insurance History Determines How Quickly Rates Rise

Your insurer will typically review your Motor Vehicle Record (MVR) at policy renewal, which means changes appear at your next renewal period (often 6�12 months after conviction). It generally takes about 30 days or more for a speeding ticket to affect your insurance because the conviction must be processed and added to your driving record before insurers consider it. Out-of-state speeding tickets can affect your insurance because carriers consider violations regardless of where they occurred. The exact timing and magnitude of rate increases vary by insurer and state, so checking both your state DMV website and your policy details helps you understand how a ticket will affect you. Understanding these financial consequences makes the case for fighting a ticket in court or taking defensive driving courses to avoid conviction-both strategies can protect your record and your wallet before the insurance damage takes hold.

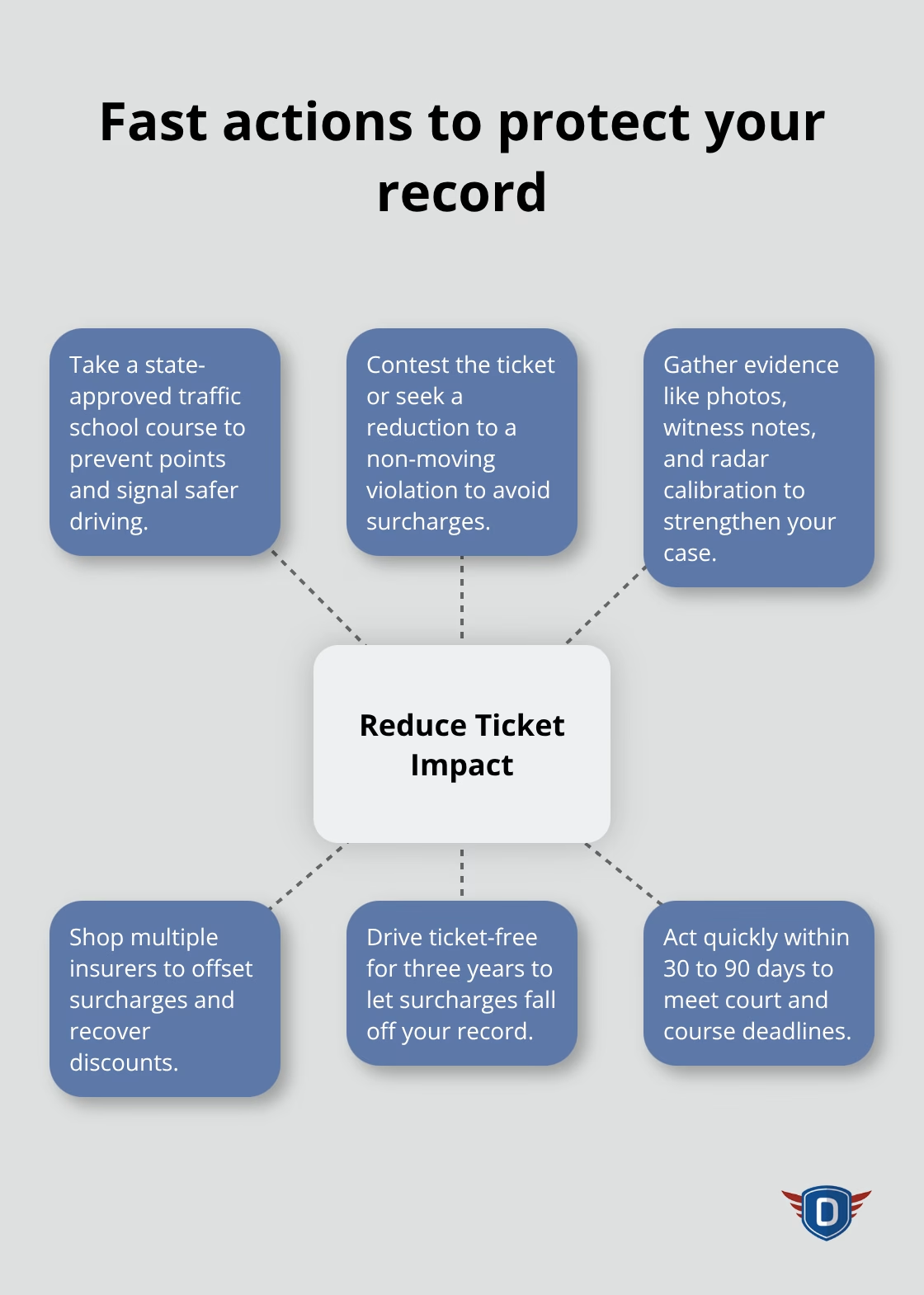

How to Stop Points From Damaging Your Record

Traffic School Courses Reduce Points Before Insurance Damage Takes Hold

Traffic school and defensive driving courses represent your most direct weapon against the financial and legal damage of a speeding ticket. Court-approved programs specifically address moving violations and help you avoid points accumulation and the insurance increases that follow. A Basic Driver Improvement course (typically four hours) sends a signal to insurers and courts that you’re serious about safer driving, which can mitigate some of the damage before your insurer reviews your record at renewal. The investment in a traffic school course typically costs between $50 and $150 depending on your state, but that cost pales in comparison to the average 23 percent insurance increase you’ll face from a single speeding ticket. Some states allow you to remove the ticket from your record entirely if you complete a defensive driving course within a specific timeframe, which means the violation never reaches your insurance company. The key is acting fast-most states impose strict deadlines for course completion, often 30 to 90 days after conviction, so delaying this step eliminates your opportunity to protect your record.

Contest the Ticket in Court to Eliminate Points Entirely

Fighting the ticket in court or negotiating with the prosecutor offers another pathway to preventing points and insurance damage, though success depends on the strength of your case and local court practices. If you contest the ticket and win, the conviction disappears from your record entirely, eliminating both the points and the insurance surcharge. If you lose but negotiate a reduction to a non-moving violation or equipment violation, the ticket may not trigger insurance increases because many carriers don’t penalize non-moving violations. An attorney specializing in traffic law costs between $500 and $1,500 for a speeding ticket case, but this investment becomes worthwhile if the alternative is years of elevated insurance premiums. The timing matters significantly-the longer you wait to contest a ticket, the weaker your case becomes because evidence degrades and witness memories fade.

Gather Evidence to Strengthen Your Defense

Your best defense involves collecting documentation about the speed limit signs, road conditions, and visibility on the day you received the ticket, which directly challenges whether the officer’s radar reading was accurate or whether you truly violated the speed limit. Photos of the location, witness statements, and maintenance records for the radar equipment all strengthen your position in court. Choosing not to fight the ticket and simply accepting the conviction means accepting years of financial damage, which explains why many drivers view the legal challenge as a worthwhile investment rather than an expense.

Prevent Future Violations to Protect Your Entire Record

Consistent safe driving habits protect your entire record from further deterioration, because a second speeding ticket within three years multiplies your financial consequences exponentially. One violation costs you roughly an average of 23 percent in insurance increases, but two violations within three years can push your premium up significantly according to insurance data. The cumulative effect matters because insurers view repeat violations as a pattern of risky behavior rather than a one-time mistake. Staying ticket-free for the next three years allows your current violation to age off your insurance record, which restores your rates to normal levels and eliminates the financial penalty entirely.

Final Thoughts

A speeding ticket creates a domino effect that extends far beyond the initial fine. Points accumulate on your driving record, insurance rates spike for years, and the financial damage compounds with each additional violation. The speeding consequences you face depend on your state, the severity of the violation, and how quickly you take action to protect your record.

The most effective strategy involves preventing future violations entirely. One ticket costs you roughly 23 percent in insurance increases over three years, but a second ticket within that same period multiplies the damage exponentially. Safe driving habits protect your entire record and your wallet, while fighting a ticket in court or completing a traffic school course can eliminate points before they damage your insurance rates.

Driver education plays a vital role in breaking the cycle of violations and protecting your long-term safety. At floridadetscourse.com, we help drivers reduce points, meet court requirements, and qualify for insurance discounts through our Florida-approved traffic school programs. Visit floridadetscourse.com to explore how our courses can protect your record and support your commitment to safer driving.